Industry

Should You Accept Rewards Cards if You Don’t Have to? Only Your Data Knows

November 14, 2025

November 14, 2025

Grace Greenwood

Grace Greenwood

Grace Greenwood

Visa and Mastercard may soon reach a settlement with US merchants around interchange costs. Interchange—the fee merchants pay to issuers every time they swipe a customer’s payment card—is a hot topic, especially as average rates have increased to nearly 2% in recent years. Everyone’s talking about this potential settlement, with Wall Street Journal even claiming the decision could “change the rewards landscape” long term.

So what’s changing and how did we get here?

Back in 2005, US merchants filed a class action lawsuit against Visa and Mastercard over excessive interchange rates. After two decades of back and forth, a settlement is on the table that would give merchants the authority to pick which specific card products they want to accept from Visa or Mastercard. This upsets the current all-or-nothing policy, whereby accepting one card brand means accepting all associated card products, from basic debit to premium rewards.

This choose-your-own-adventure landscape offers merchants an opportunity to optimize their payments mix to block or surcharge the individual high-cost card products cutting into the issuer and network’s revenue. Sounds easy, yeah?

Come off it. We’re talking about payment processing costs; you know it’s not that simple.

Cost-Benefit Analysis

Blocking or surcharging expensive cards may help with interchange costs, but such a decision comes with some undeniable drawbacks:

Irritated customers

Lost revenue

Higher churn

Irritated Customers

Rewards cards are huge in the United States. Customers willingly pay high annual fees just for the pleasure of collecting and cashing in on rewards. How many rewards they earn directly correlates to how much they spend using the card in question. In other words: to optimize rewards and recoup the costs of annual fees, a customer will pay with their rewards card whenever possible. They might even choose where they shop based on who accepts their card.

The cards with the highest interchange rates are those with the greatest rewards and consequently, the most loyal cardholders. Blocking or surcharging these cards could drive customers into the arms of your competition.

Lost Revenue

If a customer gets to checkout and you don’t accept their top-of-wallet card, they don’t just get frustrated, they walk away without spending money! Locked in revenue disappears in an instant, and a customer you spent good money attracting and guiding through your sales funnel slips away. To make matters worse, higher tier card products are typically associated with higher average order values (AOVs), so that missed revenue opportunity could be a true business loss. For recurring or subscription businesses, that loss is further compounded when you consider the lost lifetime value (LTV) for each rejected customer!

Higher Churn

If you have a recurring or subscription business model and store customer card details on file, you likely have many high-cost rewards cards in your vault right now. Should you decide to take advantage of the Visa/Mastercard settlement and restrict your accepted card mix, you will be throwing away some of those vaulted credentials the next billing cycle. You can always contact these customers to request they update their payment method on file, but that level of friction can be enough to make a customer second guess their subscription altogether.

Practical Data Analysis

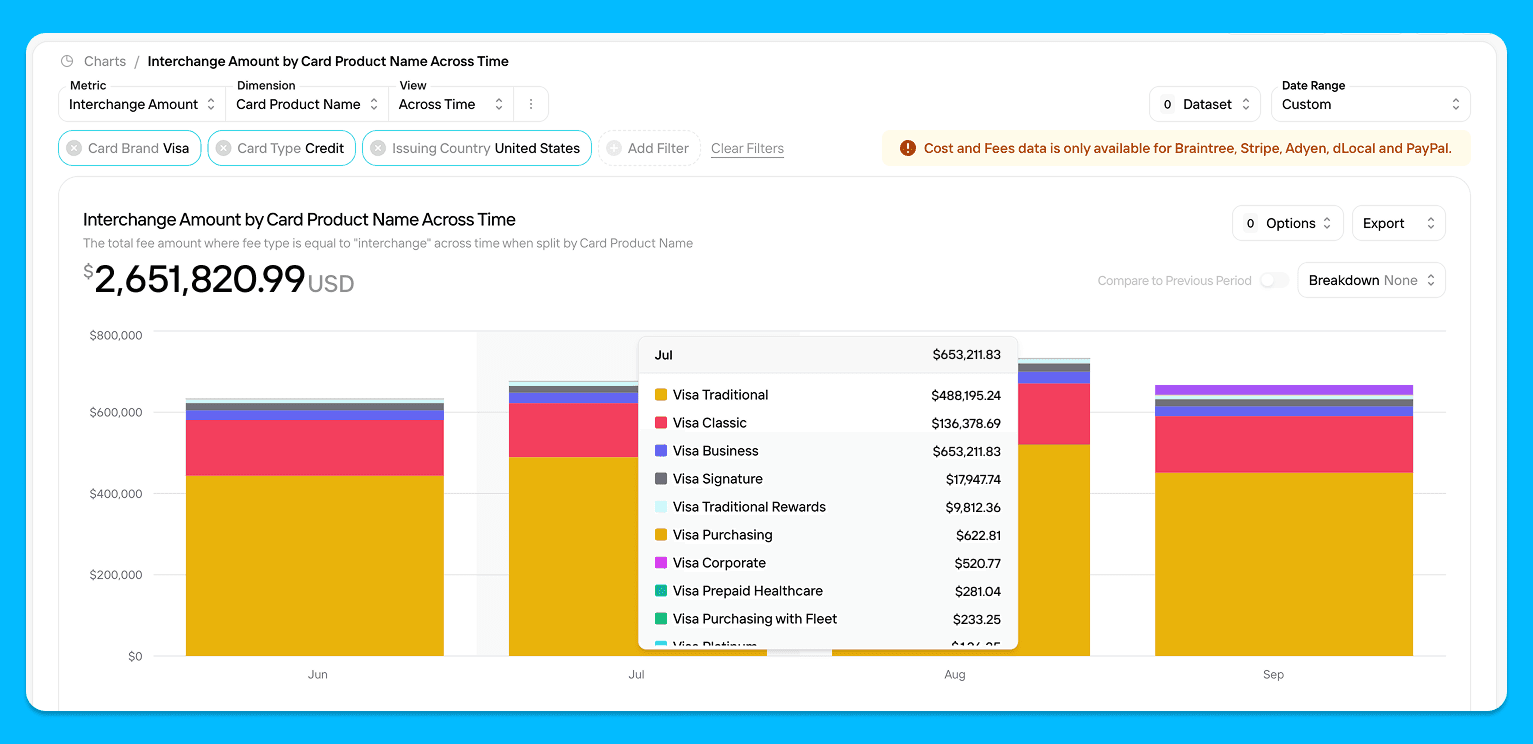

We wouldn’t be Pagos if we didn’t include some real data to back up our discussion points. Let’s take a look at one enterprise merchant’s Visa credit card transaction volume, broken down by card product over a four month period (Jun-Sept 2025) in Pagos Insights. Starting with Interchange fees, we immediately see something interesting: the majority of their interchange costs don’t come from premium rewards cards, but from Visa Traditional and Visa Classic cards.

This makes sense. Those products are more common among the merchant’s customers, and therefore generate more volume. But it shows that rewards cards aren’t necessarily the top driver of interchange costs.

The highest cost premium cards for this merchant are Visa Business, Visa Signature, and Visa Traditional Rewards cards. If this merchant did choose to block those three cards to cut costs, they’d have missed out on over $8.2 million in approved transaction volume in this four month window alone.

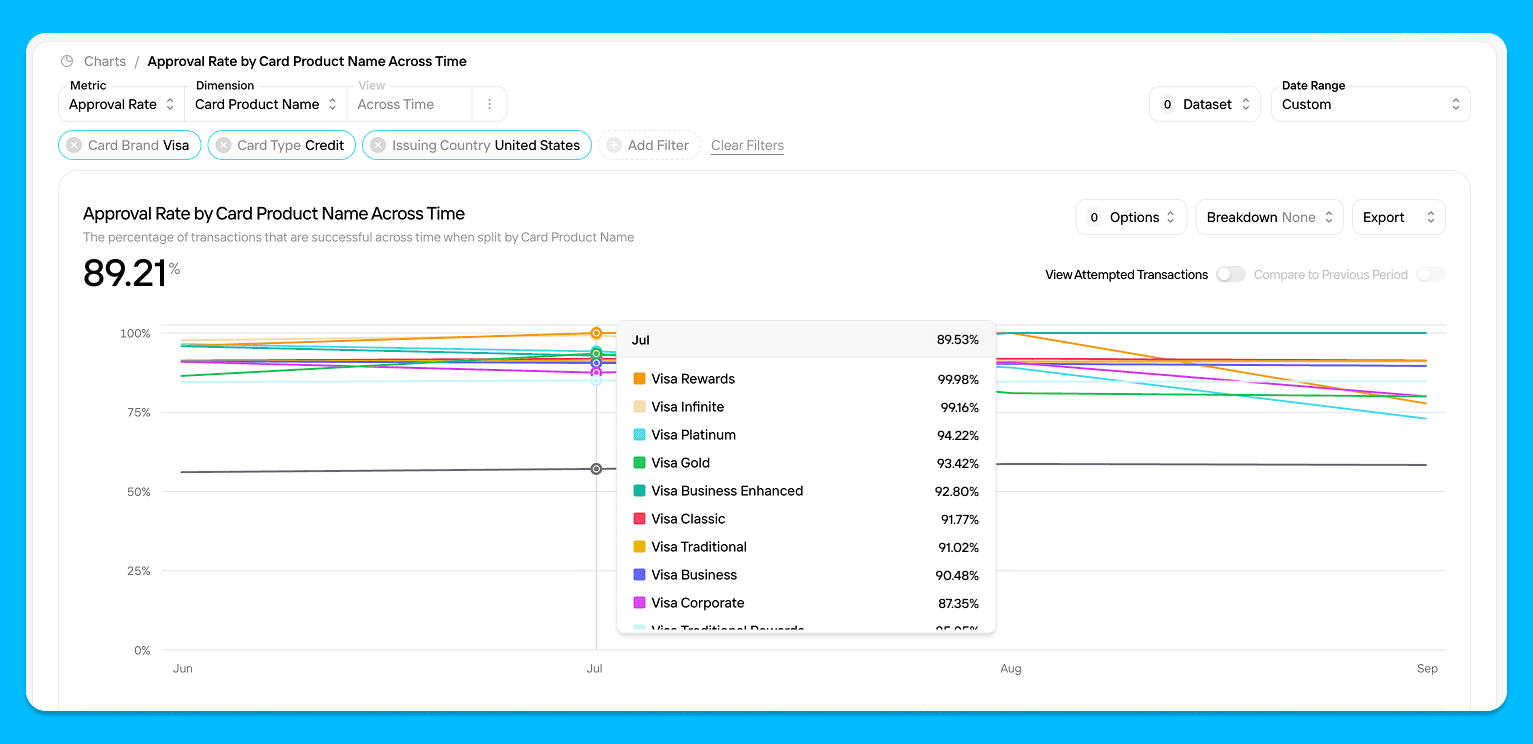

To confirm our assumptions around approvals on premium cards, we charted out approval rate by card product for that same time period:

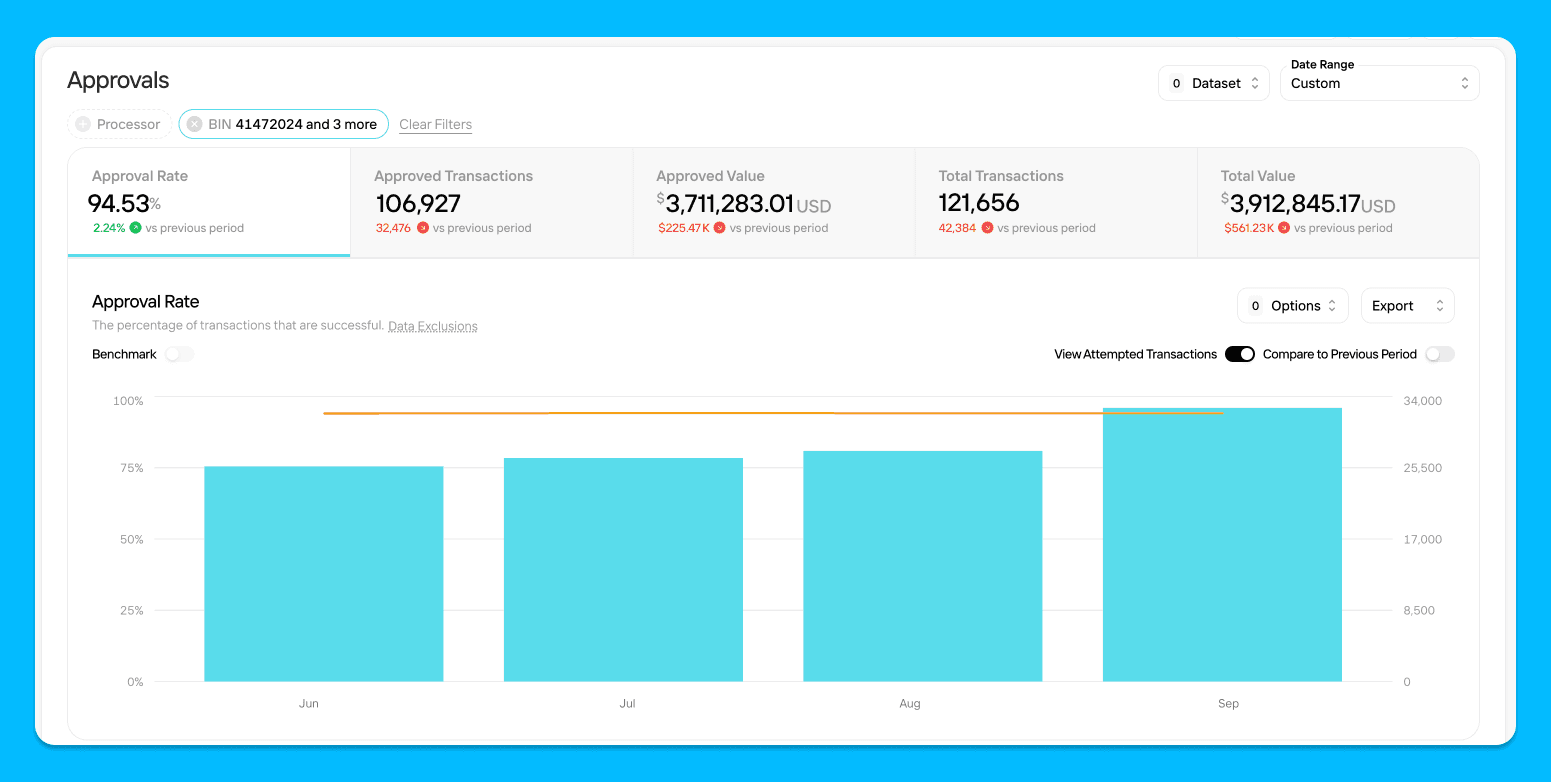

While the overall Visa credit card approval rate for this merchant is quite high (89%), it’s significantly higher for the premium cards they might be tempted to block. If we narrow down our approval rate analysis even further to the BINs associated with one of the highest cost card products—the Chase Sapphire Reserve credit card—we see a consistent approval rate higher than 94% for $3.9 million in approved revenue:

This analysis makes one thing clear: the most expensive cards aren’t always the most costly to your business. When approval rates and revenue are strong, even higher interchange rates might be worth it. Only your own data can show you where the tradeoffs lie!

Taking Action

While the final terms of the Visa and Mastercard settlement are still pending, now’s the time to start thinking about what you would do if you could reject or surcharge specific card products. As the cost of payments acceptance continues to rise, adapting your payment method mix to save up to 10 basis points on interchange rates might be worth pursuing. Notice our use of the word “might.”

As with everything in the world of payments, let your data be your guide. What card products are generating the most interchange fees? How popular are they? Does their associated AOV and approved transaction volume more than make up for processing costs—not to mention LTV of the customer? What corner of the market or segment of customers will you alienate by blocking specific card products?

If and when this settlement goes into effect, we’ll be ready with the insights you need to make smart decisions for your business. And if you want to start digging in now, we’re ready when you are. Contact Pagos today!

Visa and Mastercard may soon reach a settlement with US merchants around interchange costs. Interchange—the fee merchants pay to issuers every time they swipe a customer’s payment card—is a hot topic, especially as average rates have increased to nearly 2% in recent years. Everyone’s talking about this potential settlement, with Wall Street Journal even claiming the decision could “change the rewards landscape” long term.

So what’s changing and how did we get here?

Back in 2005, US merchants filed a class action lawsuit against Visa and Mastercard over excessive interchange rates. After two decades of back and forth, a settlement is on the table that would give merchants the authority to pick which specific card products they want to accept from Visa or Mastercard. This upsets the current all-or-nothing policy, whereby accepting one card brand means accepting all associated card products, from basic debit to premium rewards.

This choose-your-own-adventure landscape offers merchants an opportunity to optimize their payments mix to block or surcharge the individual high-cost card products cutting into the issuer and network’s revenue. Sounds easy, yeah?

Come off it. We’re talking about payment processing costs; you know it’s not that simple.

Cost-Benefit Analysis

Blocking or surcharging expensive cards may help with interchange costs, but such a decision comes with some undeniable drawbacks:

Irritated customers

Lost revenue

Higher churn

Irritated Customers

Rewards cards are huge in the United States. Customers willingly pay high annual fees just for the pleasure of collecting and cashing in on rewards. How many rewards they earn directly correlates to how much they spend using the card in question. In other words: to optimize rewards and recoup the costs of annual fees, a customer will pay with their rewards card whenever possible. They might even choose where they shop based on who accepts their card.

The cards with the highest interchange rates are those with the greatest rewards and consequently, the most loyal cardholders. Blocking or surcharging these cards could drive customers into the arms of your competition.

Lost Revenue

If a customer gets to checkout and you don’t accept their top-of-wallet card, they don’t just get frustrated, they walk away without spending money! Locked in revenue disappears in an instant, and a customer you spent good money attracting and guiding through your sales funnel slips away. To make matters worse, higher tier card products are typically associated with higher average order values (AOVs), so that missed revenue opportunity could be a true business loss. For recurring or subscription businesses, that loss is further compounded when you consider the lost lifetime value (LTV) for each rejected customer!

Higher Churn

If you have a recurring or subscription business model and store customer card details on file, you likely have many high-cost rewards cards in your vault right now. Should you decide to take advantage of the Visa/Mastercard settlement and restrict your accepted card mix, you will be throwing away some of those vaulted credentials the next billing cycle. You can always contact these customers to request they update their payment method on file, but that level of friction can be enough to make a customer second guess their subscription altogether.

Practical Data Analysis

We wouldn’t be Pagos if we didn’t include some real data to back up our discussion points. Let’s take a look at one enterprise merchant’s Visa credit card transaction volume, broken down by card product over a four month period (Jun-Sept 2025) in Pagos Insights. Starting with Interchange fees, we immediately see something interesting: the majority of their interchange costs don’t come from premium rewards cards, but from Visa Traditional and Visa Classic cards.

This makes sense. Those products are more common among the merchant’s customers, and therefore generate more volume. But it shows that rewards cards aren’t necessarily the top driver of interchange costs.

The highest cost premium cards for this merchant are Visa Business, Visa Signature, and Visa Traditional Rewards cards. If this merchant did choose to block those three cards to cut costs, they’d have missed out on over $8.2 million in approved transaction volume in this four month window alone.

To confirm our assumptions around approvals on premium cards, we charted out approval rate by card product for that same time period:

While the overall Visa credit card approval rate for this merchant is quite high (89%), it’s significantly higher for the premium cards they might be tempted to block. If we narrow down our approval rate analysis even further to the BINs associated with one of the highest cost card products—the Chase Sapphire Reserve credit card—we see a consistent approval rate higher than 94% for $3.9 million in approved revenue:

This analysis makes one thing clear: the most expensive cards aren’t always the most costly to your business. When approval rates and revenue are strong, even higher interchange rates might be worth it. Only your own data can show you where the tradeoffs lie!

Taking Action

While the final terms of the Visa and Mastercard settlement are still pending, now’s the time to start thinking about what you would do if you could reject or surcharge specific card products. As the cost of payments acceptance continues to rise, adapting your payment method mix to save up to 10 basis points on interchange rates might be worth pursuing. Notice our use of the word “might.”

As with everything in the world of payments, let your data be your guide. What card products are generating the most interchange fees? How popular are they? Does their associated AOV and approved transaction volume more than make up for processing costs—not to mention LTV of the customer? What corner of the market or segment of customers will you alienate by blocking specific card products?

If and when this settlement goes into effect, we’ll be ready with the insights you need to make smart decisions for your business. And if you want to start digging in now, we’re ready when you are. Contact Pagos today!

Visa and Mastercard may soon reach a settlement with US merchants around interchange costs. Interchange—the fee merchants pay to issuers every time they swipe a customer’s payment card—is a hot topic, especially as average rates have increased to nearly 2% in recent years. Everyone’s talking about this potential settlement, with Wall Street Journal even claiming the decision could “change the rewards landscape” long term.

So what’s changing and how did we get here?

Back in 2005, US merchants filed a class action lawsuit against Visa and Mastercard over excessive interchange rates. After two decades of back and forth, a settlement is on the table that would give merchants the authority to pick which specific card products they want to accept from Visa or Mastercard. This upsets the current all-or-nothing policy, whereby accepting one card brand means accepting all associated card products, from basic debit to premium rewards.

This choose-your-own-adventure landscape offers merchants an opportunity to optimize their payments mix to block or surcharge the individual high-cost card products cutting into the issuer and network’s revenue. Sounds easy, yeah?

Come off it. We’re talking about payment processing costs; you know it’s not that simple.

Cost-Benefit Analysis

Blocking or surcharging expensive cards may help with interchange costs, but such a decision comes with some undeniable drawbacks:

Irritated customers

Lost revenue

Higher churn

Irritated Customers

Rewards cards are huge in the United States. Customers willingly pay high annual fees just for the pleasure of collecting and cashing in on rewards. How many rewards they earn directly correlates to how much they spend using the card in question. In other words: to optimize rewards and recoup the costs of annual fees, a customer will pay with their rewards card whenever possible. They might even choose where they shop based on who accepts their card.

The cards with the highest interchange rates are those with the greatest rewards and consequently, the most loyal cardholders. Blocking or surcharging these cards could drive customers into the arms of your competition.

Lost Revenue

If a customer gets to checkout and you don’t accept their top-of-wallet card, they don’t just get frustrated, they walk away without spending money! Locked in revenue disappears in an instant, and a customer you spent good money attracting and guiding through your sales funnel slips away. To make matters worse, higher tier card products are typically associated with higher average order values (AOVs), so that missed revenue opportunity could be a true business loss. For recurring or subscription businesses, that loss is further compounded when you consider the lost lifetime value (LTV) for each rejected customer!

Higher Churn

If you have a recurring or subscription business model and store customer card details on file, you likely have many high-cost rewards cards in your vault right now. Should you decide to take advantage of the Visa/Mastercard settlement and restrict your accepted card mix, you will be throwing away some of those vaulted credentials the next billing cycle. You can always contact these customers to request they update their payment method on file, but that level of friction can be enough to make a customer second guess their subscription altogether.

Practical Data Analysis

We wouldn’t be Pagos if we didn’t include some real data to back up our discussion points. Let’s take a look at one enterprise merchant’s Visa credit card transaction volume, broken down by card product over a four month period (Jun-Sept 2025) in Pagos Insights. Starting with Interchange fees, we immediately see something interesting: the majority of their interchange costs don’t come from premium rewards cards, but from Visa Traditional and Visa Classic cards.

This makes sense. Those products are more common among the merchant’s customers, and therefore generate more volume. But it shows that rewards cards aren’t necessarily the top driver of interchange costs.

The highest cost premium cards for this merchant are Visa Business, Visa Signature, and Visa Traditional Rewards cards. If this merchant did choose to block those three cards to cut costs, they’d have missed out on over $8.2 million in approved transaction volume in this four month window alone.

To confirm our assumptions around approvals on premium cards, we charted out approval rate by card product for that same time period:

While the overall Visa credit card approval rate for this merchant is quite high (89%), it’s significantly higher for the premium cards they might be tempted to block. If we narrow down our approval rate analysis even further to the BINs associated with one of the highest cost card products—the Chase Sapphire Reserve credit card—we see a consistent approval rate higher than 94% for $3.9 million in approved revenue:

This analysis makes one thing clear: the most expensive cards aren’t always the most costly to your business. When approval rates and revenue are strong, even higher interchange rates might be worth it. Only your own data can show you where the tradeoffs lie!

Taking Action

While the final terms of the Visa and Mastercard settlement are still pending, now’s the time to start thinking about what you would do if you could reject or surcharge specific card products. As the cost of payments acceptance continues to rise, adapting your payment method mix to save up to 10 basis points on interchange rates might be worth pursuing. Notice our use of the word “might.”

As with everything in the world of payments, let your data be your guide. What card products are generating the most interchange fees? How popular are they? Does their associated AOV and approved transaction volume more than make up for processing costs—not to mention LTV of the customer? What corner of the market or segment of customers will you alienate by blocking specific card products?

If and when this settlement goes into effect, we’ll be ready with the insights you need to make smart decisions for your business. And if you want to start digging in now, we’re ready when you are. Contact Pagos today!

Share this Blog Post

Share this Blog Post

Let's Chat on

Want to dig deeper into payments data, news, and insights? Have hot takes of your own?

We're talking all things payments on Reddit.

Latest Blog Posts

Subscribe to our Blog

Subscribe to

our Blog

Subscribe to our Blog

By submitting, you are providing your consent for future communication in accordance with the Pagos Privacy Policy.

Let's Chat on

Let's Chat on

Want to dig deeper into payments data, news, and insights? Have hot takes of your own?

We're talking all things payments on Reddit.