Company

Monitor Your VAMP Risk Exposure with Pagos

With the launch of the new Visa Acquirer Monitoring Program (VAMP), Visa is making (ongoing) formidable changes to how they track and measure risk across their network. For online merchants processing a large volume of card-not-present transactions, it introduces new formulas, new thresholds, and a broader definition of what counts against you. With this shift, you may need to rethink how you analyze your Visa transaction data.

To help you keep up, we’ve introduced changes to the Chargebacks Metrics dashboard within Pagos Insights. We now calculate chargeback rate for Visa transactions using the new VAMP formula and present your chargeback volume in such a way as to reflect Visa’s own risk assessments. This not only demonstrates where you stand against Visa’s tightening thresholds, but takes the guesswork out of sorting VAMP out all on your own.

Quick VAMP Review

VAMP replaces Visa’s older Fraud Monitoring and Dispute Monitoring Programs. As of this blog's publication date, here’s what we know: instead of tracking fraud and chargebacks separately, VAMP rolls both into a single rate, calculated as the sum of all chargebacks and early fraud warnings, divided by your settled card-not-present transaction count. Chargebacks are found on your TC15 report, while early fraud warnings appear on TC40.

There are a couple things to keep in mind about this new calculation:

TC15 identifies all chargebacks, both fraud and non-fraud. This means even if your disputes are driven by non-fraud reasons (e.g. product quality issues, customer confusion, or processing errors), they now fit into Visa’s new definition of “risky behavior” and will count against your VAMP rate.

If a transaction appears on TC40 as an early fraud warning and again on TC15 as an actual fraud chargeback, it’s counted twice in your VAMP rate.

Visa excludes any disputes resolved through Rapid Dispute Resolution (RDR) and pre-dispute tools (e.g. Verifi or Compelling Evidence 3.0)

Visa also adjusted their new VAMP thresholds as follows:

Region | Disputes | Excessive Rate |

|---|---|---|

US, Canada, EU, & Asia Pacific | 1,500+ | 220 BPS |

LAC | 1,500+ | 150 BPS |

CEMEA | 150+ and $75,000+ | 220 BPS |

Pagos Gives You the Full Picture

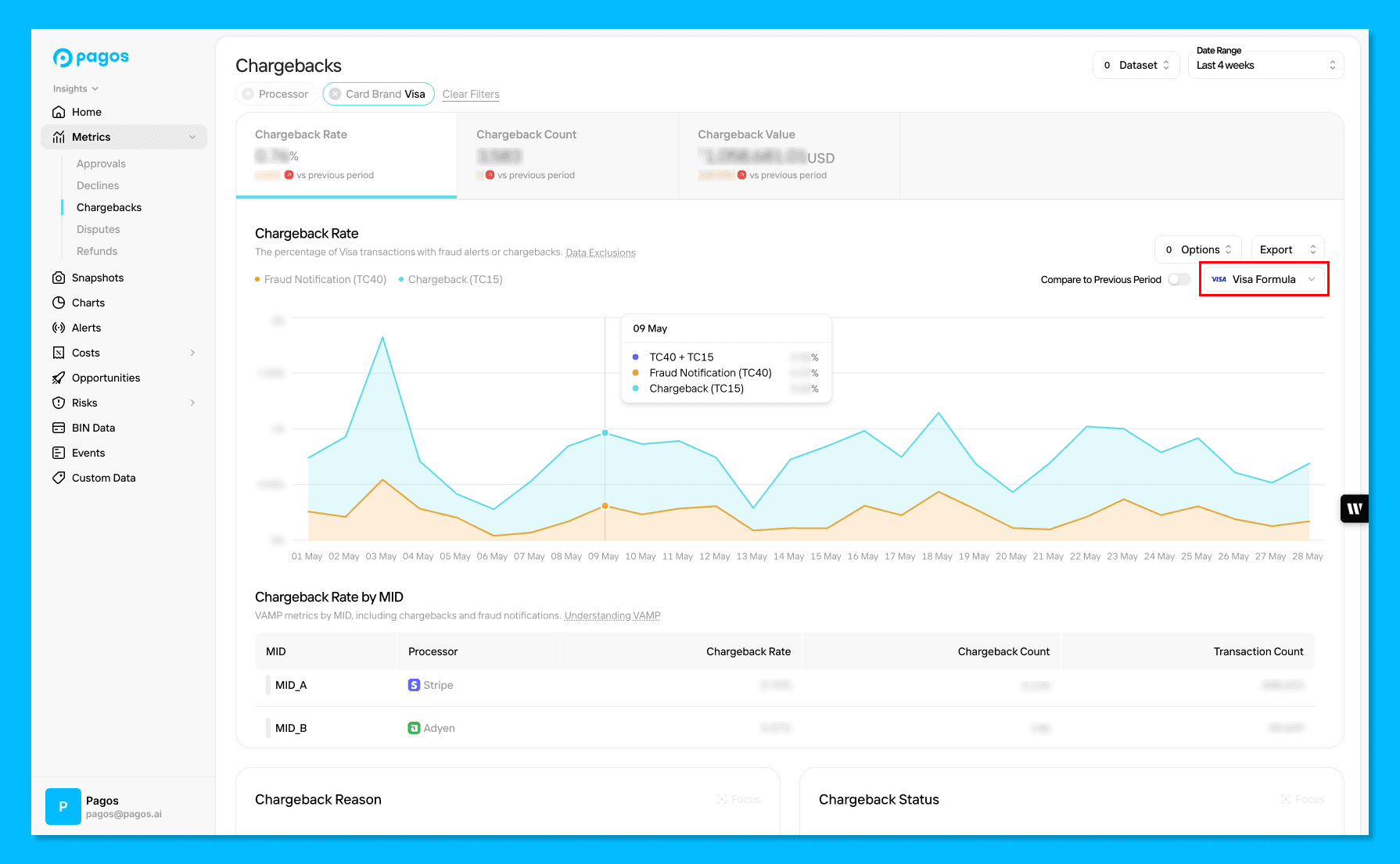

In the Chargebacks Metrics dashboard of Pagos Insights, you can select which formula you want us to use when calculating your chargeback rate. When you select the Visa Formula, the dashboard filters to only include Visa card-not-present transactions, and calculates your chargeback rate using the combined count of TC40 fraud reports and TC15 chargebacks. You can even see the official contributions of each to your overall chargeback rate over time:

Keep in mind: At this time, only Adyen and Stripe provide the TC40 data necessary to calculate the VAMP chargeback rate accurately. If you ingest data from other processors into Pagos, you’ll see a warning on this page alerting you of your incomplete data. Keep checking back, however, as we’re always working on adding new data ingest sources for TC-40 data, including from Visa/Verifi directly.

Stay Ahead of the October Deadline

Visa’s stricter thresholds start taking effect in October 2025, and by April 2026, the excessive ratio drops from the current rate of 2.2% to 1.5% in most regions. Pagos can help you track your VAMP rate and take action before your processor or Visa flags you for risky behavior. Whether you need to download Visa chargeback data, feed it into internal tools, or trigger workflows when fraud alerts come in, we make it easy to stay compliant and responsive.

One more important thing Pagos can do for you with regards to VAMP: keep up with ongoing changes from Visa. We’re closely monitoring every new announcement out of Visa and are adapting Insights’ capabilities to match.

With Pagos, you don’t have to guess how VAMP will impact you or scramble to calculate your VAMP chargeback rate on your own. Ready to explore the Chargebacks Metrics dashboard? Contact us today!

By submitting, you are providing your consent for future communication in accordance with the Pagos Privacy Policy.